Why the Tories' "put people to work" growth strategy has failed

Why the Tories' "put people to work" growth strategy has failed

Even with high immigration, the workforce can't grow enough to compensate for catastrophic failure of innovation and capital investment.

What do you do when your economy is in the doldrums and you need to kickstart growth?

Why, you put more people to work, that’s what you do.

This has been the Tories’ strategy since 2010. The sustained attack on welfare benefits has all been focused on “making work pay” - encouraging, and at the margin forcing, people with illnesses, disabilities and caring responsibilities into paid work.

But there is another way of putting more people to work, and that is to import them.

A new report says immigration has failed to generate growth

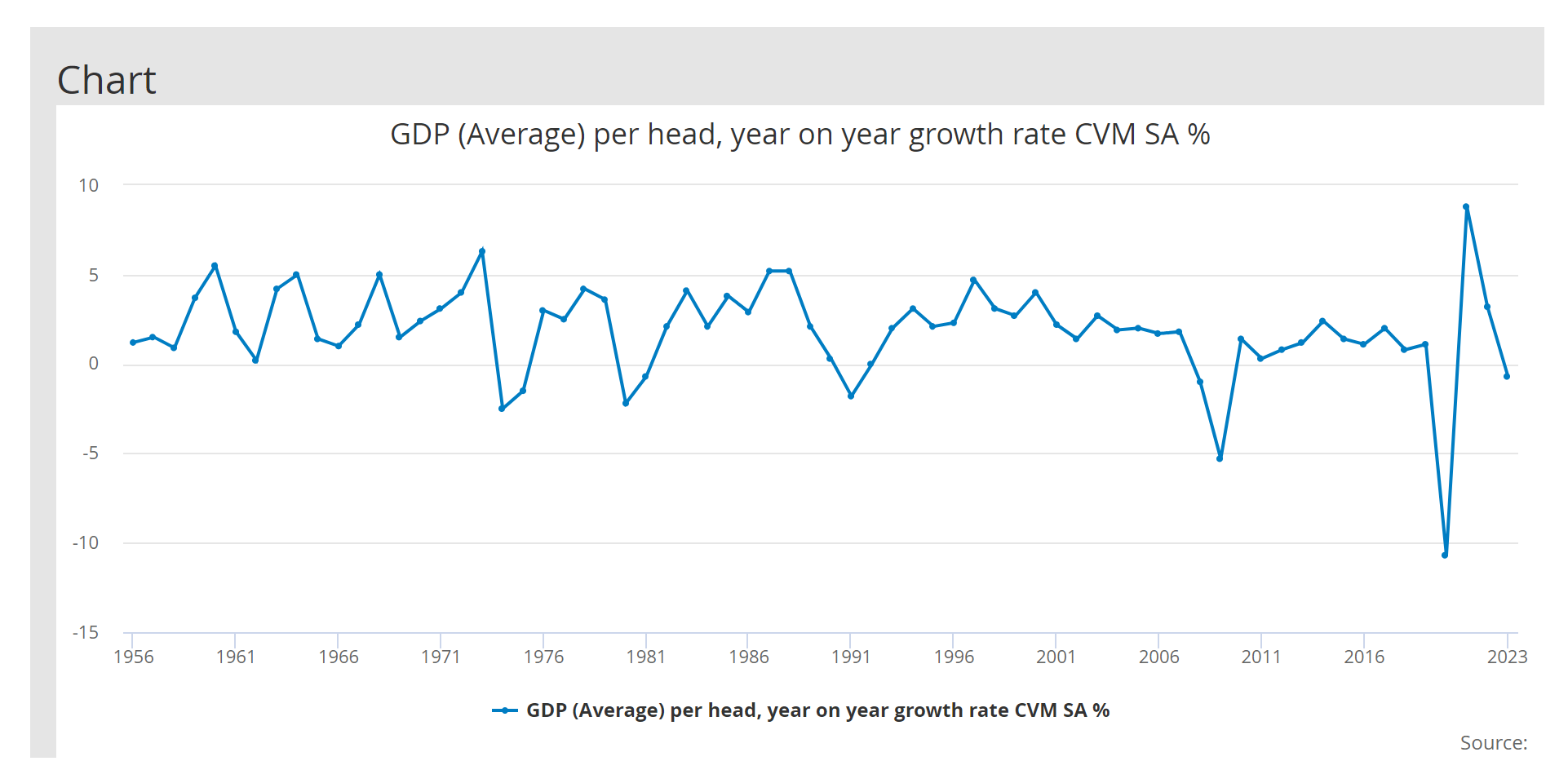

In a new report, the centre-right CPS thinktank says that importing people to kickstart growth has been the unspoken strategy of successive governments since 1997. And it argues that the strategy has manifestly failed. Since 2010, GDP per capital growth has fallen off a cliff:

The dramatic collapse in GDP per capita shown in this chart clearly isn't caused by immigration. It's pretty obviously the result of the 2007-8 GFC. Indeed, if we look at the year-on-year growth rate of GDP per capita, the collapse due to the 2008 banking crisis is even more obvious:

GDP per capita shrank by 5% on a year-on-year basis. At the time, it was the worst collapse of GDP per capita since World War 2.

Note what happened next. There was a rebound, but not to previous growth rates. Between 2010 and 2020, GDP per capita growth remained stuck at 1-2% per annum. (The dramatic movements since then have of course been due to the Covid lockdown and an energy crisis.)

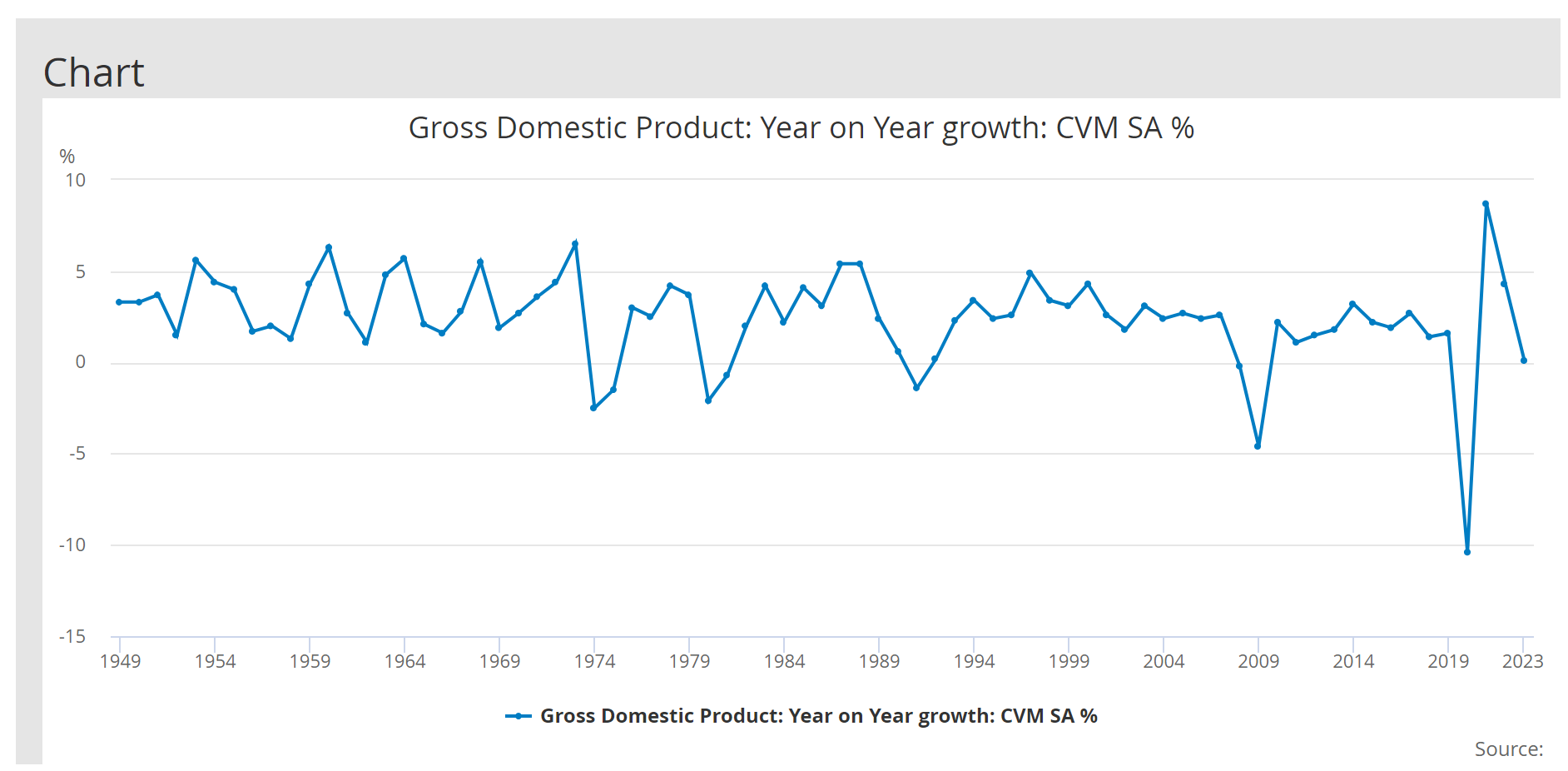

Jenrick & O’Brien want to blame the stagnation of GDP per capita after the financial crisis on rising net migration. On a “lump of GDP” basis, this makes sense: more people means less GDP per person, obviously. But as this chart shows, total year-on-year GDP growth remained lower after the financial crisis than before:

Even without high net migration, therefore, GDP per capita would have stagnated.

The UK economy fundamentally changed after the financial crisis

Jenrick & O’Brien argue that since high immigration hasn’t kickstarted strong GDP growth, we’d be better off without high immigration. But we don’t have a counterfactual. We don’t know what GDP growth would have been if immigration had been lower during the post-crisis years. To what extent was GDP growth supported by post-crisis immigration?

It’s hard to say, but this chart gives us a clue. MFP - the contribution of what we might loosely call “innovation” - to gross value-added (GVA) growth collapsed after the financial crisis. GVA growth has been persistently far below historic levels ever since. This chart appears to indicate that increasing labour contribution to GVA partially offset the MFP collapse:

We have to be careful about causation here. The chart does not show that the rising labour contribution caused the collapse of the MFP contribution, nor that it prevented it from recovering. All we can say for certain is that for reasons we don’t know, UK GVA has been supported by rising labour contribution in the post-crisis years.

This chart also doesn’t show that cheap immigrant labour has been substituting for capital investment, as Jenrick & O’Brien suggest. The contribution of capital to GVA started falling in 1998, but labour contribution also fell. The real pre-crisis story was one of rampant innovation, not labour substitution. And both labour and capital contribution have risen since the financial crisis - inevitably, given the utter failure of MFP.*

What this chart really shows is that after the financial crisis, the UK’s GVA switched from being primarily innovation-led to being driven principally by a lot of people doing a lot of work. We don’t know why this is, and it is very concerning for the UK’s long-term prospects: economies that rely primarily on a large and very hard-working labour force to drive GVA don’t tend to be either rich or advanced. But it is difficult to see why rising immigration would cause such a dramatic change. Surely, something else must be going on.

Without a satisfactory explanation of why MFP happened to fall off a cliff at precisely the same time as the worst economic crisis since World War II, it is frankly insane to imagine that the pre-crisis level of MFP contribution could be restored simply by cutting immigration.

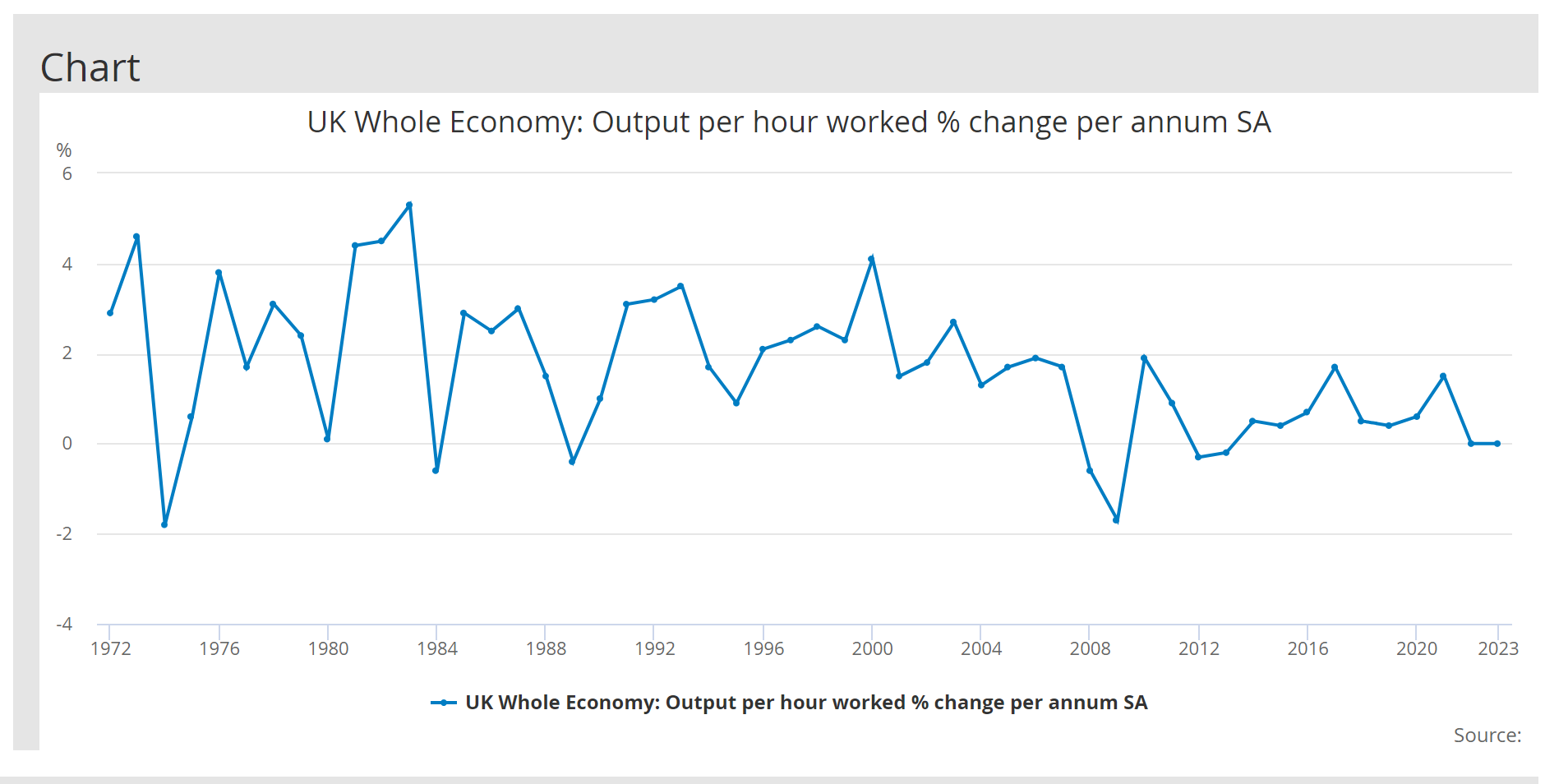

Of course, an increasing labour contribution doesn’t necessarily mean a larger workforce. Workers could simply be producing more per hour. But labour productivity fell sharply in 2008 and, despite an initial rebound, has not recovered:

Clearly, the UK’s economic growth since the financial crisis has relied primarily on workforce growth.This comes from two sources:

UK residents being forced into work through benefit cuts (including state pension age rises) and sanctions

Immigration

Of the two, the second is probably more significant.

The counterfactual must therefore be that without rising immigration, both GDP growth and GDP per capita growth would have been lower, though we don’t know by how much. So Jenrick and O’Brien’s claim that rising immigration has failed to deliver growth is not true. It just hasn’t been able to offset all the forces depressing GDP since the financial crisis.

“Workforce QE”

When GVA growth relies principally on the size of the workforce, you can stimulate growth by adding more people. We could call this workforce QE, or “QE of the people”. When you want to increase output, you open the doors and let immigrants flood in: when you are at capacity, you close the doors to new immigrants and encourage existing ones to return whence they came.

This seems to be how Jenrick and O’Brien think of immigration. They complain that immigration hasn’t kickstarted growth, and that it has unfortunate side effects such as pressure on housing and public services, poor integration and cultural tensions. These complaints bear a striking resemblance to those made of monetary QE: it didn’t kickstart growth, and it had unfortunate side effects such as high asset prices (including housing), rising inequality and social strains.

At the individual business level, adding more people to increase output and laying off any that are surplus to requirements looks like a no-brainer. But the economy as a whole doesn’t work like that. A strongly growing economy usually needs more workers, not fewer, to prevent inflation taking off, so sending immigrants home could make inflation worse. And an economy that is on the floor usually has high unemployment, so needs fewer workers, not more. If you turn on the immigration taps to “kickstart growth”, you might crowd out the local unemployed, making it harder for them to find jobs.

However, there could be a solution. Just as in monetary QE the type of asset purchased matters, so in workforce QE, the type of people you add to your workforce matters. If you mainly add low-skilled people, then you are more likely to crowd out the local unemployed, and you will also skew your workforce towards lower skills,: in economics, this is known as “hysteresis”, and it depresses productivity, which over the longer term is a drag on growth. But if you mainly add high-skilled people, they are less likely to crowd out the local unemployed - indeed, may even create jobs for them - while the increase in the general skill level of the workforce should mean higher productivity and hence, over the longer term, higher growth. This is the thinking behind “points-based” immigration systems designed to “bring in the skills the economy needs.”

The skill levels of people coming into the workforce matters on the demand side too. Higher-skill people tend to command higher wages and thus have greater purchasing power, so if the general skill level of the workforce increases, aggregate demand should also increase - though if skills improvement doesn’t feed through into higher productivity, higher aggregate demand could simply result in higher inflation. Conversely, if the workforce increase mainly consisted of low-skill people, who tend to have low wages, aggregate demand would be likely to fall, just as it does if unemployment rises.

The benefit reforms since 2010 have brought people into the workforce who, for a variety of reasons, mainly do low-skill jobs and are poorly paid. There is therefore hysteresis in the UK-resident workforce as a direct consequence of government policy. There’s also hysteresis from the UK’s ageing population, not because older people are less skilled but because they are more likely to be hampered by health problems and caring responsibilities: this might help to explain the longer-term downward trend in the UK’s labour productivity. And there is a more familiar form of hysteresis too, namely people who are slipping down the skills ladder because technological change has rendered their skills obsolete and they lack the time, money or incentive to develop new skills.

The fact that since 2010 UK productivity has been well below its pre-crisis trend suggests that immigration has not compensated for this multi-factor hysteresis, nor for whatever other factors might be depressing labour productivity: insufficient GP and dentist appointments, long NHS waiting lists, traffic jams, lack of affordable childcare…the list is long, and growing.

For those who, like Jenrick & O’Brien, believe that restricting low-skill immigration and favouring high-skill is the road to future prosperity, the points-based system introduced in the wake of Brexit is not working properly. We are importing far too many people, and far too many of them are low-skilled. In their minds, “Workforce QE” must be reformed to ensure that only high-skilled people can come here, and that when they are no longer needed, they leave. Putting down roots and building a life here is for the birds. How this solves the problem of poor integration and cultural tensions is a mystery.

If the UK had high unemployment, there might be a respectable argument for restricting immigration in low-skill sectors to prevent crowding-out of British workers - though enforcing employment rights and minimum wages for immigrants might be just as effective.

But the UK doesn't have high unemployment. The story of the last few years has been one of low unemployment coupled with persistent shortages of both high- and low-skill workers, especially in sectors such as health and social care where pay is poor and stress sky-high. The government has tried to ease these shortages by selectively relaxing immigration restrictions. Clearly, the economy needs more workers, both high- and low-skilled, than the resident workforce can provide. High-skilled workers could perhaps be trained, though in medicine the lead time is long and the pay is poor. But where are we going to get low-skilled workers from, if not from immigration?

There is a widespread belief that if we ended low-skill immigration, “all those unemployed young people” would pick up the slack. Sadly this fails on simple mathematics. There just aren’t that many unemployed young people. Or, indeed, people of any age. Attempts by successive governments to cut immigration significantly have all failed due to the same fundamental problem: the British workforce isn’t large enough to fill all the jobs the UK economy generates, so British workers choose the jobs they want to do and the gaps are inevitably filled by immigrants. For British workers, this seems rather a good deal. Why are people complaining?

Nevertheless, the belief that there is a large pool of low-skilled British workers ready and willing to be deployed into crucial sectors to replace the foreigners refuses to die. Jenrick & O’Brien invoke it with their notion that raising care workers’ wages by the princely sum of 40p per hour will attract enough British workers into the sector to eliminate most immigrants - though they don’t seem to have thought about how the current employers of those British workers might respond to worker flight. And the radio host Rachel Johnson hailed Rishi Sunak’s proposal for all 18-year-olds to do a year’s ‘National Service’, which for the majority would mean spending one weekend in four doing unpaid community service, on the grounds that “we need more fruit pickers.” Dear Rachel, fruit picking isn’t community service, it’s work, and like all work that people are obliged to do, it should be paid.

The fact is that there is no “reserve pool” of British workers, low-skill or otherwise. If there is one thing the present government could celebrate, it is its remarkable success in getting people into work. The UK is at full employment, and has been for best part of a decade. The real problem is the structural shift in the economy since the financial crisis. Even with high immigration, the workforce simply cannot grow enough to compensate for the failure of innovation and capital investment.

Weak stimulus is better than no stimulus

Like monetary QE, Workforce QE is a weak stimulus. In the absence of supportive fiscal policy, it can’t “kickstart growth” as Jenrick and O’Brien would like. All it can really do is stop GDP growth from grinding to a halt. But that’s not a reason to abandon it. After all, some growth is surely better than no growth.

Right now, trying to cut immigration is a very bad idea. It will depress GDP and, because of the UK’s tight labour market, add inflationary pressures to the economy. Rather, we should investigate the reasons for the structural shift that has rendered economic growth dependent on an ever-growing labour force. Why has wage growth been persistently poor despite full employment? Why has the UK suffered such severe and long-lasting negative effects from the 2008 financial crisis? Why has capital investment in the UK, both private and public sector, been utterly dismal for such a long time? And crucially, what effect has this had on productivity, which as any fule know is the the real driver of GDP growth?

If we address these questions instead of chasing populist chimeras, we may be able to come up with sensible policies for reforming the UK economy.

Related reading:

Bifurcation in the labour market

We need to talk about productivity

Image: Migrant farm worker, New York. By David Shankbone - David Shankbone (own work), CC BY 2.5, via Wikimedia Commons.

*MFP is a residual. It is the difference between total GVA and the contributions of labour (adjusted for quality) and capital. In this handy guide, the ONS explains it thus:

In the real world, changes in MFP can arise for a number of reasons including technological progress, economies of scale, changes in management techniques and business processes or more efficient use of factor inputs. MFP is linked, therefore, not to an increase in the quantity or quality of measured factor inputs but rather to how they are employed. In practice, MFP may also reflect measurement error of inputs and outputs. For example, if a firm employs new forms of capital that are not captured in our statistics, we would likely underestimate the growth of capital services and this could materialise as overestimation of MFP.

Some writers have suggested that the collapse of MFP reflects the UK’s shift to services, particularly digital services whose outputs are hard to measure. This would be a compelling argument were it not for the fact that MFP fell so dramatically in the financial crisis and did not recover. For this reason, I think the answer to the UK’s MFP failure more likely lies in the financial sector.

Wasn't the collapse in UK GDP/capita growth after 2007 driven as much by the decline in North Sea oil and gas production as by the GFC?